I am one of those quants that is generally cautious of the tyranny of the mean. Averages are clearly useful for understanding how normative levels change (if at all) as a function of different inputs or groupings. They also, unfortunately, often hide the interesting parts of the underlying distributions of data upon which they are based.

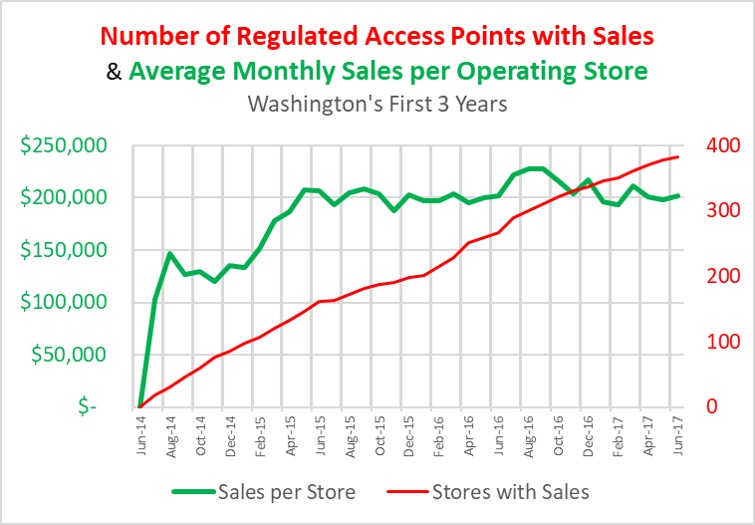

With that caveat, and with a ridiculously surprisingly small amount of associated verbiage, I would like to present to you two similar charts summarizing retail sales over the first three years of State-legal Retail Cannabis sales in Washington State.

I’ve been quietly tracking this for awhile now, largely in response to a comment made by a Seattle Retailer about a year and a half ago. That comment was something to the effect that “a retail store requires annual revenue of at least $2 million in order to survive”. I thought that was a bit of an over-generalization (e.g., it is likely more expensive to run a leased store in Seattle than an operator-owned store in a rural setting), but it did pique my interest.

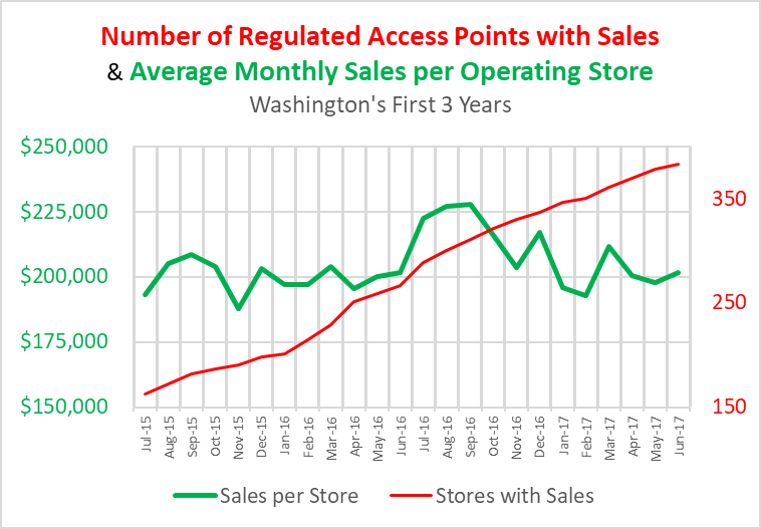

Each of these two charts shows both the number of Retail Access Points that were actively selling product each month and the average (pre-tax) PER-STORE sales of Cannabis, Cannabis extracts, and Cannabis-infused products that occurred each month.

The first chart shows all three years of Washington’s State-legal Cannabis market. The second chart zooms in on the most recent two years. I added the second chart in order to draw attention to how flat the AVERAGE per-store monthly revenue has been since about July of 2015 …. when the excise tax was shifted to it’s current 37% “at retail only” version. I am inferring no cause/effect relationship here.

Two charts … and no more text from me. I’d love to hear what you think of what these charts show (and imply) via comments on this post. I will try to be responsive to all comments.

Dramatic pause before we zoom into the last two years.

It appears we have not yet reached a point of store saturation in the state as additional stores still increase sales overall. We can only aspire to seeing as many cannabis outlets in Washington as there are Starbucks (559) but we sure beat the heck out of them in per store ($110K/mo) and per square foot revenue! With a cost of goods hovering around 35% it seems that an average store, unlike the average producer, should be quite profitable. If a store at 200K/Month in revenue is not very profitable then the owner needs to really look hard at what is going on.

Steve — agreed re: store saturation.

With the fall of per-unit pricing over the past couple of years, it is also clear that open store, while selling the same number of dollars per month ON AVERAGE are also selling quite a few more units of product per month ON AVERAGE than they were previously.

The 280e tax hit decreases their profitability (significantly), but I tend to agree with your last statement anyway.

That’s a great What, Jim, but getting to the Why requires a dash of observation and a heavy dose of speculation. OK – I’ll bite. Here goes…

1. The overall marketplace (Total Sales $) continues to rise with the increase in store count. This indicates an expansion of the marketplace. Could it be that same-store-sales are micro-regional, and more stores are opening up more micro-regions? Or, could it be that with time, social taboos are dropping like flies, and more people are taking advantage of the opportunities available to them? Impossible to tell without more data.

2. Sales are seasonal. There are pronounced bumps between June and October in both 2015 and 2016, which miraculously coincides with the phenomenon known as “Summer” in Western Washington. Consumption increases with the sun, and then flattens back out as the sun fades. Could it be that there is simply more to do during these months, and consumption is activity related? Speculation here can easily go in a hundred different directions. More on this in a moment.

3. Sales fall precipitously in November in both years. I suspect this is related to tightening inventories due to fall outdoor harvest not quite making it into the stores yet. Less selection, and possibly, higher prices? Then we see sales bounce back for Christmas, and then eventually level out. This could indicate that the market demand exceeds the supply during the late fall, and then supply catches up.

4. Average per-store sales tanked from Dec 2016 to Feb 2017. This is one of the more interesting points in the distribution. Why? Did the ever increasing store count suddenly exceed the off-season market demand, perhaps indicating that we have too many stores for the softer off-season? Did the fall harvest that got rain-soaked fail to show up in stores until March? Did stores use this time period to sock away money (and therefore purchase less and sell less) for IRS taxes due in April, causing a negative bubble like November?

5. What happened in Feb 2015? Something stepped hard on the accelerator.

SteveO – thank-you for your thought-provoking comment.

In summary — I don’t know.

There are definitely “micro-regions” emerging. These seem to be, largely, a function of the way the LCB geographically allocated access points coupled with the various placement restrictions (state rules and local zoning/ordinances). One example that comes to mind is the Stone Way area in Seattle where OZ and #Hashtag are located …. more stores have opened locally. Up near Bothell, the B-E highway used to have one store near the north end, but quickly built up to a cluster of 4 or 5. 4th Ave South in Seattle comes to mind (lots of examples).

Loved your Summer comments … Hempfest is likely also causative (thank-you Vivian et al).

There is definitely a repeatable signal for seasonality. One of them is that the December-to-February pattern that is fairly clear in 2016-17 is also evident (just lower amplitude of oscillation) in the 2015-16 period.

I also like to speculate as to why …. and appreciate any and all speculations/opinions/observations as to what repeatable seasonal patterns are emerging and why. I think your comment captures a good deal of the what and provided some thoughts on the “why” that are clearly not superficial. Thank-you for that. Would love to hear what others think …. reading folks’ thoughts on these may inspire a way to use the extensive data that exist on this market to differentiate between options.

Finally … what happened in Feb 2015? Without referring to data, my best guess would be that production capacity finally took off just as stores became reasonably accessible (geographically) to many more Washingtonians and the competition/supply dynamics led to reductions in prices at retail from the originally-ridiculous ones (ridiculous, that is, when compared to what the norm was in the still-functioning Green Cross Access Points).

Oh yah, the police started aggressively shutting down Green Cross access points around then — betcha that was a biggy in determining the pulse in per-store sales.

Complex dynamic processes are a hoot to model.

Again … thanks for the thought and time you put into your comments.