Earlier this week, one of the local drug interdiction task forces infesting the state announced the bust of 32,449 plants (and some cash and gold and a few houses and people) estimated to be worth $80,000,000.

In using a $2,465 per plant valuation, these asset-forfeiture specialists are, apparently, assuming this to be the level of pricing that WA-produced product is expected to command on the streets of non-legal states craving product of the quality produced in the Pacific Northwest.

I am glad that these heavily armed and armored folk have shared a current Black-market pricing estimate with us. It may prove informative to Washington’s Legislators as they wrestle with the true fiscal risk of the WSLCB’s gross mismanagement of our state’s regulated Cannabis marketplace.

I recently posted that approximately 1.2 million regulated plants were initiated in Washington between May and July of this year. Those plants have now, for the most part, been harvested during a period where the WSLCB has no real-time access to an integrated source of the traceability data that comprise their seed-to-sale tracking capability. 1.2 million plants are coming to market, just as the LCB is “Cole-memo-blind”.

So, Legislators …. The WSLCB currently can’t really track 1.2 million plants, whose worth on the Black market, according to the boys with the armored personnel carriers, falls just shy of THREE BILLION DOLLARS. That is 3 Billion dollars of potentially taxable product. Product that can now be diverted out of state with relative ease. Product being harvested and cured and processed and packaged and sold by hundreds of businesses that your laws and the LCB’s incompetent over-regulation are squeezing to the edge of fiscal oblivion.

If only 25% of those plants were diverted to the out-of-state Black market, they would have the potential to bring $750,000,000 of untaxed (free) revenue to the farmers and processors (and retailers?) of the state. That would pay quite a few mortgages and grocery bills and health insurance premiums.

However, since the LCB can’t track it (diversion) or measure it (diversion), one can reasonably guess that it (diversion) is not happening. Never mind … go back to planning for your short legislative session and upcoming efforts to be re-elected. Read the LCB’s recent bullshit so-called “study” relating to regulatory options for the Homegrow of Cannabis. Then go to sleep comforted that all is good and that those regulators down on Pacific Avenue have things as well in hand as they would have you believe.

In the meanwhile, what is actually happening right now is that a surge of more than 350 tons of fall-harvest WA-produced Cannabis is in the process of making it’s way to market (which market is debatable) This pulse of product is expected to put further downward pressure on prices that can be expected by wholesalers choosing to sell within the regulated market.

As Legislators interested in tax revenue, you should not, for example, be surprised to see the price of the average gram of finished flower being sold at wholesale falling to as little as $2.50 per gram within the next month or two.

That decline will, in turn, likely cause downward pressure on retail pricing and a resultant reduction in collected taxes. As prices plunge downward, the relative benefits increase of selling elsewhere with better prices.

Sleep well, Legislators.

From the farmer’s perspective, this is not all doom and gloom. There will definitely be increased downward pressure on prices being paid to farms and processors over the next few months. At the same time, it is clear that there are products (and farms) out there that are commanding decent prices in this difficult market.

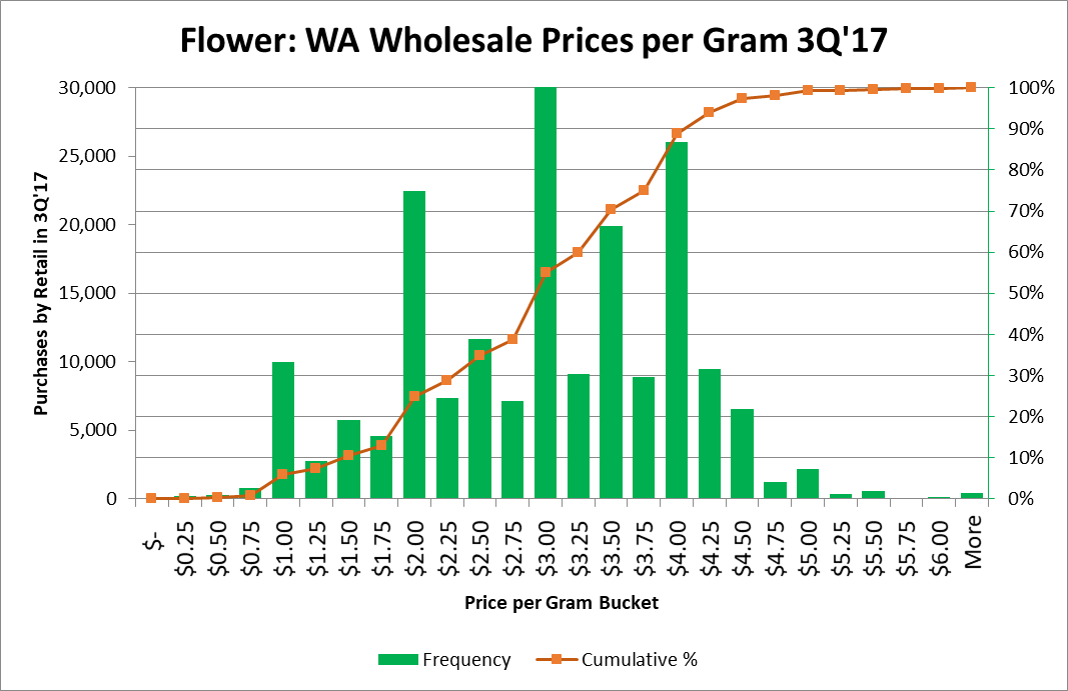

Here is a distribution of the wholesale prices paid by retailers for flower in the 3rd quarter of 2017. This chart shows the count of distinct manifest transfers into retail for flower that occurred during the 3 months ending September. To clarify, in the following chart, if a given manifest included 3 different strains of joints each priced at $2.00 per gram, that would represent three of the 22,000 “transfers” that are counted in the “$2.00 per gram” price bin.

The line superimposed over the frequency distribution gives the cumulative density of the chart (e.g., 60% of the flower transfers into retail during 3Q’17 were sold at or below the price of $3.25 per gram).

Two things worth note on this chart are the very human propensity to price things at whole number levels ($1, $2, $3, or $4 per gram, for example) and the fact that there is, indeed, some flower out there that is able to command almost Black-market-like prices when sold into retail.

Presumably this $4+ per gram flower represents good stuff. In fact, I’d argue that the wholesale price commanded by flower is one of the best indicators available of the “quality” of the product being sold (and bought) within the regulated system.

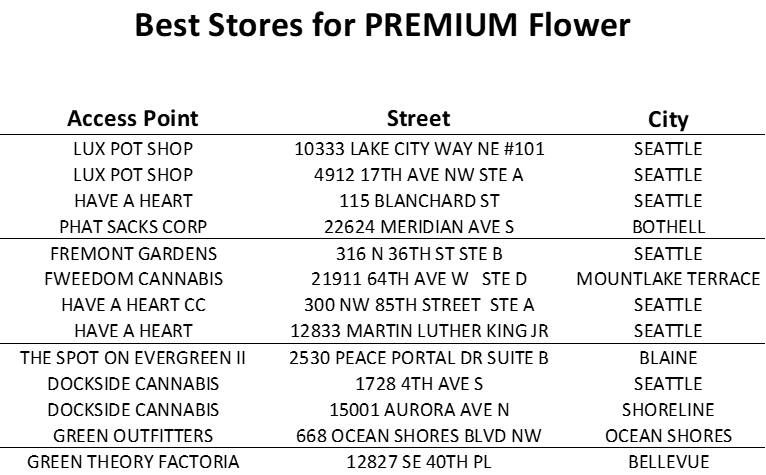

With that in mind, I leave you with the following list of stores apparently stocking the best Legal Cannabis in the State (without sharing much of my methodology … as this stuff is kinda proprietary).

After categorizing each wholesaler into a number of distinct categories (Ranging from “Value” to “Premium”) based on the distribution of prices their flower commanded in 3Q, I derived a number of distinct groupings of Retail Access Points based on the proportion of their 3Q flower purchases that came from farms (and processors) in each pricing category.

The list above is the segment that corresponds to stores that appear to be spending not only time and effort, but MONEY to ensure that the flower they are offering their customers is of the best quality. I manually over-rode the segmentation and removed 3 stores from the list (for different, but relevant, reasons that I will not bore you with).

In 3Q, there were less than 500 pounds of flower sold into retail by wholesalers considered to be “Premium” in my model. The listed stores stocked a disproportionate share of their shelves with product from “Premium” and/or “High-Priced” suppliers.

It is interesting that none of these “best flower stores” are East-side stores.

I feel fortunate that I live in the greater Seattle area (as nice as I’ve found Spokane and most folks that I’ve met from the area to be).

It is also interesting that some of the good, solid players that made it over from the old “Green Cross” days are represented on this list. Dockside and Have-a-Heart (for example) are stores that, today, can reliably produce the Certificate of Assessment (testing result sheet) for product upon customer request. They were always among the best for Patients. Now they are among the best for folks wanting the best.

Given their presence on this list, they can point you to quite a few of the BEST examples of flower that are available in the regulated marketplace today. I would imagine the same can be said of the other products they stock, but that is just a guess at this point.

If you want to purchase the best flower in the state that you can get legally (specifically, that for which the farmers are paid the most) you will not go wrong shopping at these stores.

Please remember, however, that Cannabis is a Schedule-1 restricted drug that the Federal Government considers illegal and that the elf running the DOJ seems to think is bad for you and for us all. Please do not view this post as an encouragement to shop for Cannabis, let alone to shop for it in a regulated retail access point. Take it for what it is, a listing of the stores that seem to be curating their flower offerings — and investing in the offerings of the best of the suppliers out there — to a much greater degree than their peers.

If I were the type of person to shop in a State-Legal Retail Cannabis Access Point, I would not hesitate to shop in these stores. Note that none of these stores either paid me for being on this list or, for that matter, even know they are on it (yet). Let them know …. They should be proud of how they are sourcing their product. They are, by this simple metric, the best stores in the state (from the perspective of any consumer in search of the best flower being produced in the state).

Let them know you appreciate what they are bringing to you. They are NOT like the other 390-odd stores currently operating out there. They are, IMHO, “better” on this basic dimension. There are other “good” stores out there … but these are the best (on this simple measure).

If more stores were willing to pay a decent price to the farms of this state, less of the $3 Billion dollar Black-market potential of the current harvest would be at risk of going “Cole-rogue” and of putting everything that the LCB would like to have us think they have been working toward at increased risk (much as their lack of seed-to-sale tracking capabilities currently does).

Thank God for Pie-Hoe!

Note to Retailers – The work I’ve done that underlies the list of the “best stores” at the end of this post would likely be of substantial utility to those of you that wish to up your purchasing game. Let me know if you are interested. It’ll cost you.

Jim,

I have to call BS on your simplistic assumption that Most Expensive = Highest Quality. For so many reasons.

For example, and without getting into a religious war over outdoor vs. indoor, we all know that by and large, outdoor product is less expensive overall per unit volume. So, you have just (inadvertently?) relegated outdoor products to less than High Quality status, simply because they are cheaper to produce. I find that to be less than true.

Also, many (most? all?) of the stores on your list are big-bucks stores that can afford to buy Expensive Weed and carry it. This is not a small point, because it is the intersection of much smaller retail marketplace with Minimum Order Quantities (MOQs) that conspire to make Expensive Weed so difficult for smaller stores to carry. The store has to buy relatively large quantities to even get any weed at all from many of these Expensive P/P suppliers, and then suffer through much less than fast turnover on the shelves, because such a small percentage of customers want to pay those high prices.

There is also the suffrage of fancy branding being placed on ordinary weed to sell it for Expensive Weed prices in a fancy package. A very famous country music singer comes to mind….

High Quality Weed can be obtained now at almost any price level. If the weed has been carefully grown (and properly flushed and cured), pesticide free, fertilizer free, hand trimmed, and packaged simply, it can be Awesome Weed at a moderate or even budget price.

Smaller boutique stores can be a great source of Awesome Weed grown by Tier 1 and 2 P/Ps that simply can’t supply the volume that W@lmart sized stores require. Small batch and carefully crafted is seldom carried by the churn and burn stores, and doesn’t need to cost $4+ per gram in today’s market.

In my mind, that actually makes these stores better than those carrying large amounts of Expensive Weed, because they are better serving the consuming customers out there today who are demanding High Quality AND Price Point.

OK, Steve. While I respect your opinion, do you truly think that the price that retailers pay for product is not related to the quality of that product?

Independent of that, is there anything out there in the data reflecting products, their status and their sale that you think might serve as a better index of quality?

One stylistic suggestion. Referring to simplistic assumptions as bullshit is, in itself, bullshit. Particularly when the assumption has merit.

Jim,

Yes, I do in fact believe that price and quality are not by definition tied together – maybe in a perfect market, but not in ours. Just to echo what others have said, there is definite change happening in the marketplace, wherein some P/P’s are having a difficult time getting their high quality product into stores, and have resorted to blatant price cuts to gain interest. I have seen many examples of great weed at discount prices where the quality exceeds by far what is delivered by the more well-known brands at much higher prices. This is why I challenged your assumption rather strongly.

I do find great value in the data distribution you posted, especially as it shows how small the more expensive market really is as a percentage of the overall total. If you had similar data from a year ago, it might be good to compare, especially at the lower price end of the market, as that is where all the movement is happening in the past 6 months.

Regarding other metrics of quality, I do terribly wish that we had some independent metric, perhaps like USDA grades for beef. But if we do, I don’t know what they are. I don’t think our industry is that mature yet. So, how do we measure quality? Certainly not THC %. We can’t smell the product because of the closed packaging. We can, in most circumstances see the product (unless the packaging is so bad, but that’s another issue). So, we look for color, crystals, whether the bud looks like what it is supposed to look like (tight, loose, etc), trim quality, what pesticides (if any) or fertilizers (if any) are labeled, and we add what we know from the QA analysis and from the farmer about how they raise the product (by conversation, and by visiting the farm). I just don’t know how you turn such subjective analysis into an industry wide objective measure at this point. As an industry, we need further maturation before we can do that. But cost as a measure of quality? Hardly.

As for me calling BS on your assumption, and my lack of style points on the issue, I bow to the style that you have clearly shown over time – I can’t compare. You data analyses are always interesting. But in this case, I felt that the fundamental underlying assumption is very, very wrong, and needed to be called out. No shade on your work, just your assumption. And no, there is no self interest here at all – I’ll happily PM you the details. My ONLY interest is in educating others about what is happening in our marketplace today, especially in the last 3-6 months. It has changed a lot, but the why’s and wherefore’s are for another thread.

SteveO — I appreciate your thoughtful response and the constructive way in which you coined your criticism.

My use of price per gram paid for flower by retailers as a measure of “quality” is not an assumption. It is an operational definition.

You are one of a number of people that have challenged my “assumption” (it has been treated as overly-simple, amusing, overly-broad and -I believe- biased by different commenters both here and on the 502Cannabis forum).

My training as an Experimental Psychologist involved efforts to measure things (the psyche) that are arguably not directly observable. One of the things I was trained to do in such situations was to look for things that COULD be measured that might provide a reasonable window into the construct being investigated.

As such, please know that my use of wholesale per-gram prices as a metric associated with the concept of QUALITY is not an assumption that price = quality. It is an OPERATIONAL DEFINITION in which wholesale price-per-gram (and a number of related derivations … such as the categorizations of wholesalers into mutually exclusive and exhaustive groups and the subsequent categorization of retailers based on their purchase patterns across these wholesaler groups) is used as an index or metric thought to relate to the not-directly-measurable entity called QUALITY.

One of the benefits of using operational definitions is so that the ball can be moved forward. The lack of a well-defined measurement scale that unambiguously captures the various attributes that constitute “quality” need not stop investigations into the concept of “quality”.

One of the other benefits of using operational definitions is that they are transparent and available to all. From peer researchers or analysts that might wish to replicate or build on earlier work to interested parties that see deficiencies in and, thereby, challenge and improve the definition.

Your comments, SteveO, and those of Bob and a few others on 502Cannabis are (I believe) challenges to that definition.

That is good, and I thank-you for that.

I absolutely agree that lots of things are likely relevant to “quality” other than price-per-gram. Indeed, it is logically possible that price-per-gram has nothing to do with “quality”.

However, if price-per-gram had nothing to do with “quality”, I’d argue that the market would then be either highly inefficient or highly (completely?) irrational.

For the moment, having the ability to measure Price-Per-Gram for every package-SKU for every strain for every farm across time and the ability to relate it to the purchasing of every retailer (or wholesaler) does allow the assessment of this index of “quality” in numerous ways … many of which (ironically) provide information that I believe to have the potential to shed light on the degree of inefficiency and/or irrationality present in different parts of the market.

In any case, please be aware that my analytical datasets have access to a number of indices of quality that I have been able to squeeze out of the data supplied by the LCB. These include, but go well beyond the lab-reported potency metrics.

This blog post was less an analytic discussion that a simple description of the distribution of transactions between processors and retailers involving flower in terms of the prices recently paid per gram of flower. It is a description that shows that there is flower moving at both low prices and at high prices. It is a description that shows that most flower is moving at “average” prices.

Rather than pointing out the stores on the lower end of the pricing acquisition scale, I opted to point out the ones that showed a pattern of sourcing more of their product from “high-priced” wholesalers than is typical across stores.

While I do not hold the assumption that price = quality, I DO assume that price is not independent of quality (and, further, that price reflects — amongst other things — the perceived value of the product).

I am aware that situations in which a wholesaler charges a very high price for product could be related to things other than quality.

I am also aware that situations in which a retailer PAYS a very high price for product could be related to things other than quality.

Ditto the above two comments for situations where transactions are made at very low prices.

I do not, however, wish to speculate in this forum on yet another topic that might evoke negative attention from authorities outside of this state. My discussions regarding the increased likelihood of diversion resulting from the meltdown of the LCB’s traceability oversight capabilities are about as far as I want to take such speculation..

Thanks again for your response, SteveO.

I found it helpful and informative.

Bleak future where stores only care about price – imagine if the only selection of beer and wine you had at a store was because it was ‘cheap’.

Also, kudos to those stores you listed – but there is an additional thing they are providing which was missed- they are providing value to customers. They are knowledgeable and have well trained staff that knows the difference between schwaggy outdoor and top shelf, hand trimmed, 4 week cured, primo. Some customers don’t care, they are just looking to get high. Just like some people who order a drink in a bar want well liquor because it’s cheap. But if you’ve ever worked in a bar you know the staff’s number 1 job is to upsell to higher margin items. IF bartenders didn’t do that the bar goes out of businesses. Same goes for Budtenders. Stores need to carry a selection and budtenders need to learn about why products are good, better, best and they need to upsell! You only get so many door swings, you need to make as much off each one as possible, not sell the $2 joint of the day deal to everyone that walks in.

Jamie … I doubt the future will be a place where stores care ONLY about price.

At the same time, I expect the future will be a place (as today is) where stores certainly DO care about price.

If a business does not care about price (either what they are paying or what they are receiving for whatever it is they are selling), they will not be a business for long (unless, of course, they are just a front for some criminal-like enterprise).

I have now profiled all wholesalers and all retailers on this dimension, as well as quite a few others. I expect that I will be making lists available so that the shopping public can choose not only the stores they frequent but the farms they desire in a better-informed manner. We may have a grossly inefficient market today, but that is just an opportunity to make it a wee bit more efficient. If, in doing so, it can be made more effective for the consumers and patients that are now legally required to use the regulated system, then that is some very nice cream-cheese icing on the cake.

On another note:

I intend to reply in a bit more depth to SteveO’s “bullshit” post later this week (likely on the weekend), as I’ve now looked up where his store sits on the pricing scale …. and it is in a rather extreme, outlier position (note that it was not one of the extreme outliers that I called out in the stores I listed in the post).

Over the past few days, SteveO has been posting on a related thread (or two) up on the 502Cannabis Google Groups forum. Now that I have a good feel for his company’s product acquisition pricing strategy (which seems rather extreme), it has put the rest of his posts into a different perspective.

I never ceases to amaze me how much self-interest can infest the words that emanate from one’s mouth or fingertips …. and how those self-interested words are so often the real kind of bullshit (rather than the bullshit that one calls something when people like SteveO , apparently, feel threatened).

Gotta love the transparency that data can bring to an inefficient market.

Jim,

You are a really smart guy! I was pointed to your blog by a manager of three rec stores in Washington who recognizes the rapid drop in quality due to competition and well, a whole lot of factors. None of those stores are on your best store list. I am a partner in a tier one which is slaughtering all its plants on Thursday and quitting this game due to the fact that stores are unwilling to pay a price that will let us stay in business (we calculated that we required at least 4$ a gram to keep the lights on and make a small income, which for all of us would be less than we had made in our “regular” jobs previously). We took a lot of pride in our flower and that I think, unfortunately hurt us in this market. We were receiving 4.25$ a gram for our flower for a short period of time, but the store said they wanted to move it faster so they were only willing to pay 3$ to make it more “competitive”. As we reached out to other stores, they said our product looked amazing, but then we never heard back from them because we were not willing to essentially give it to them. My understanding is that the current average price for outdoor is 27 cents a gram 1.50 for indoor (and it is expected to drop more), at that price we would make more money by throwing it in the garbage. We honestly think that other than perhaps those stores on your list, there will be no cannabis worth smoking very soon, at many stores I think they are already there. I have yet to be impressed by any of the flower recommended to me by budtenders. I always ask for their strongest strain because I smoke every evening and have a fairly high tolerance. Every single time I have been given a flower with the highest THC% they have and every time I have been unimpressed with the results, taken a couple tokes and then picked up my own flower instead.

The last store I was at gave me flower that was so wet I had to dry it for a day before I could smoke it and it reeked of wet hay from being packaged wet, it was mediocre at best. I called the store to warn them that the product could develop mold due to its moisture content, they offered me a trade for something else, I declined (I need no extra cannabis) and said I was just trying to do them a favor. I have little faith in the ability of this market to maintain a quality product if only a handful of stores will buy it. People’s obsession with everything being cheep will over rule quality in this market as it has in so many others. I also believe it is not possible to grow weed at the current market price without the use of illegal pesticides and shady growing techniques. Any way, this is a huge topic with a million intricacies that I could ramble for days about. I am of the opinion that we are essentially at the point where things need to be entirely torn down and rebuilt now or all we will have left is huge, corporate grows (maybe a few little dudes will live). These large grows will inevitably produce tainted weed in order to do things as cheap as possible and keep their investors happy.

Currently, I am advising everyone I know to avoid rec stores and get a medical card to grow their own and I want to see it become legal for everyone over 21 who wants to grow, to be able to do so. There are bad things going on in grows, at stores and with the state and the more one starts to look around at it, the more it starts to seem like a bad thriller movie. Keep up the great work! Now I’m going to look through all your other blog posts! You rock!

On a side note about the above comment by Jamie. I have met very few knowledgeable or often even friendly budtenders on my visits to stores, there are some stores that have rad crews, the store that was moving all our stuff until the price drop had awesome budtenders and I will miss them, but not the store’s buyers. A buddy of mine who works for a cannabis genetics testing company in Oregon recently came up here to visit stores and said he only met one budtender who could tell him anything about the farms where their products came from, he also mentioned that he was thoroughly unimpressed by almost all of the flower he saw and that Oregon’s rec market is currently in a rapid dive in quality and price to growers as well.

Cheers,

Bjorn

Bjorn – thank-you for your heartfelt words. I apologize for taking almost a week to respond. I have been looking closely at pesticide violation data from the LCB and have been both focused on that and in a resulting funk for the past few days. I will be posting my summary of that work on HI-Blog this morning.

I am truly sorry that you’ve had to make the hard decision to close up shop, in spite of your best (and, apparently successful) efforts to produce a high-quality, desireable crop (“fire”).

I share your concern – both as a potential consumer of regulated product and as someone that would like to see Washington’s industry thrive in the future when commerce is allowed to cross state lines.

The story unfolding (the reality in your case) does appear to be one where businesses whose business model involved producing “fire” and being paid accordingly are, differentially, being killed off by the regulatory framework under which they are forced to operate.

That is another story (or three).

Best of luck going forward. Be careful, as I suspect that the enforcement arm of the LCB (and, increasingly, those of local authorities) will be paying more attention going forward to the non-regulated industry that their destructive mis-regulation is nourishing.

I hope your genetics and skills are not lost for all time to those preferring regulated cannabis. It is possible the market will eventually change the direction in which it now appears to be headed. If consumers (and voters) demand it, it should get better. In such a world, there will be a demand for “fire”. In such a world, there will be a market for Washington cannabis in other states.

Let’s hope that consumers and, by extension, Legislators demand so soon.

Jim,

Thanks for your response. Your blog on pesticide use in the industry is very interesting and disturbing, I have directed many people I know to it already and will be posting some excerpts to my Instagram page, where I have a number of followers who are interested in such things and in seeing change in the industry. I am going to create a website and blog of my own about what is going on in recreational and medical markets in this state and country. The site/blog will also inform people about all the lessons we learned trying to make it in the industry, so that they hopefully don’t make the same mistakes. There will be organic growing tips as well and a fun little section of weird/old videos, music, art stuff for people to amuse themselves with after partaking in a hopefully non-pesticide tainted product. We have a couple experiments that we are about to do involving the industry, if the results are interesting, we will let you know them. Keep up the awesome work, I will keep watching.

-Bjorn

Thank-you, Bjorn.

I appreciate your kind words and agree that some of the ways in which this market is regulated are disturbing.

The general disdain for consumer protection displayed consistently by the LCB (notwithstanding their Red Hand of Edible Poisonousness edible labelling requirement) is disappointing at many levels.

My short list of areas most damaging to consumers caused by the LCB’s choices follows. This list shares the common trait that the actions taken by the LCB (rulemaking, allocations, enforcement priorities) which led to the listed inadequacies seem either ill-conceived and/or ill-implemented. All of the LCB’s actions are supposedly constrained and partially defined by direction from the Legislature. RCWs, WACs and the interpretation of those laws and rules by the LCB each need adjustment if the consumer risk endemic in today’s market are to be reduced. Here’s the list of LCB inadequacies most damaging to consumers (IMO):

-failing to ensure that lab QA/safety and Potency/strength testing is accurate and reasonably repeatable

-failing to ensure that product found to be impacted by issues with inaccurate(inadequate?) and/or non-repeatable(dishonest?) lab testing be recalled or in some other way meaningfully mitigated

-failing to ensure that enforcement of wholesalers focuses on dangerous growing and processing practices

-failing to ensure that enforcement of retailers holds them accountable for being able to produce all required safety information to consumers upon request (note that the rules regarding safety info were just changed, I believe … and not in the direction of increased transparency to the consumer)

-failing to order the recall of dangerous (or potentially dangerous) product

-failing to enforce against sales at levels below the cost of production

-failing to crack down effectively either vertical or horizontal integration

-regularly stacking the deck against smaller producers through rule-making, enforcement, fee structure and legislative input

-failing to have penalty options available that are consistent with the infraction (I acknowledge that this is a bit harsh of a criticism, as aligning penalties with infraction severity is difficult)

-seemingly using enforcement resources to punish licensees critical of the LCB

-allocating inadequate numbers of retail access points, failing to push legislature for law that would protect medically-endorsed retail access points (DOH-compliant ones) from local bans, moratoria, and zoning more restrictive than that faced by retail pharmacies.

Those are the biggies, off the top of my head.

Good luck with your blog … I look forward to seeing it.

Jim,

Yeah, the problems/failings are pretty intense. How much larger of a work force of responsible individuals do you think LCB would need to do things properly?

-Bjorn

Bjorn — I have my opinions about that, but will not share details as that is the type of thing the LCB should pay to be told.

Bottom line is that I believe they are adequately staffed, but have a big issue with how they allocate and prioritize their resources.